Exhibit 99.1

Corporate Presentation Fall 2021 Ticker: GCEH Exchange: OTCQX

Disclaimer This presentation contains forward-looking statements reflecting management's current assumptions, projections, expectations, targets, intentions or beliefs about future events or other statements that are not historical facts. These forward-looking statements can be identified with words such as "expects", "plans", "projects", "potential", "suggests", "may", or similar expressions. The forward-looking statements in this presentation involve known and unknown risks, uncertainties and other factors that may cause the actual results to be materially different from any future results, performance or achievements expressed or implied by such statements. Forward-looking statements in this presentation include, without limitation, statements regarding the future cost of Camelina feedstock, our ability to cultivate Camelina in forecasted amounts, the achievement of anticipated low carbon intensity scores of our products, the operation and development of our Bakersfield, California biorefinery, the market size of our products, and the availability of the capital needed to expand our refinery and related operations. For more detailed information about the risks and uncertainties that could cause actual results to differ materially from those implied by, or anticipated in, these forward-looking statements, please refer to the Risk Factors section of our Annual Report on Form 10-K and subsequent updates that may be contained in our Quarterly Reports on Form 10-Q and current reports on Form 8-K on file with the SEC. Forward-looking statements speak only as to the date they are made. Except as required by law, we do not undertake to update forward-looking statements to reflect circumstances or events that occur after the date the forward-looking statements are made. This presentation does not constitute an offer to sell or buy securities, and no offer or sale will be made in any state or jurisdiction in which such offer or sale would be unlawful prior to registration or qualification under the securities laws of any such state or jurisdiction. (i)

1. Company Overview 2. Investment Highlights 3. Business Overview 4. Appendix 2 Table of Contents

Company Overview

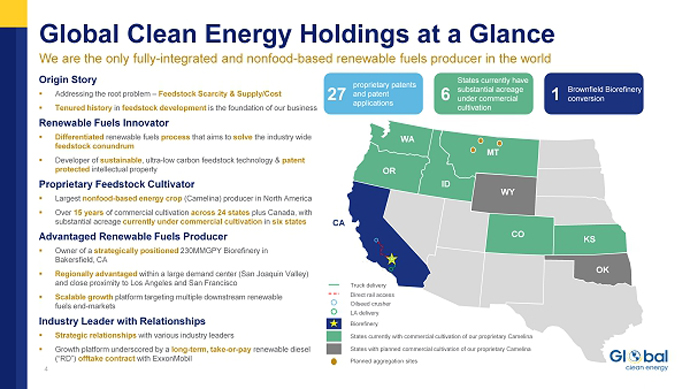

4 Origin Story ▪ Addressing the root problem – Feedstock Scarcity & Supply/Cost ▪ Tenured history in feedstock development is the foundation of our business Renewable Fuels Innovator ▪ Differentiated renewable fuels process that aims to solve the industry wide feedstock conundrum ▪ Developer of sustainable , ultra - low carbon feedstock technology & patent protected intellectual property Proprietary Feedstock Cultivator ▪ Largest nonfood - based energy crop (Camelina) producer in North America ▪ Over 15 years of commercial cultivation across 24 states plus Canada, with substantial acreage currently under commercial cultivation in six states Advantaged Renewable Fuels Producer ▪ Owner of a strategically positioned 230MMGPY Biorefinery in Bakersfield , CA ▪ Regionally advantaged within a large demand center (San Joaquin Valley) and close proximity to Los Angeles and San Francisco ▪ Scalable growth platform targeting multiple downstream renewable fuels end - markets Industry Leader with Relationships ▪ Strategic relationships with various industry leaders ▪ Growth platform underscored by a long - term, take - or - pay renewable diesel (“RD”) offtake contract with ExxonMobil CA WA MT ID OR WY CO KS OK 6 States currently have substantial acreage under commercial cultivation 27 proprietary patents and patent applications 1 Brownfield Biorefinery conversion Global Clean Energy Holdings at a Glance We are the only fully - integrated and nonfood - based renewable fuels producer in the world States with planned commercial cultivation of our proprietary Camelina Biorefinery LA delivery Oilseed crusher Direct rail access Truck delivery States currently with commercial cultivation of our proprietary Camelina Planned aggregation sites

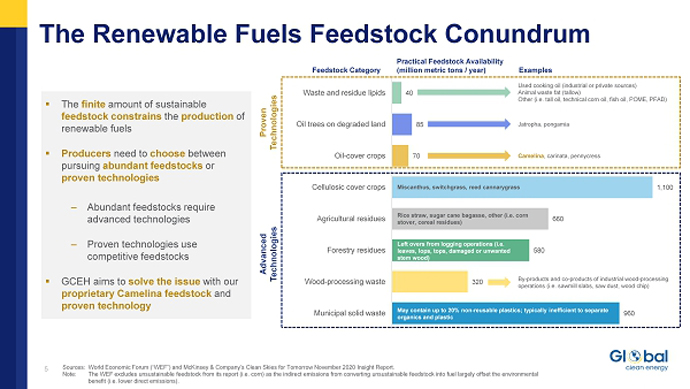

Feedstock Category Practical Feedstock Availability ( million metric tons / year) Examples Sources: World Economic Forum (“WEF”) and McKinsey & Company’s Clean Skies for Tomorrow November 2020 Insight Report. Note: The WEF excludes unsustainable feedstock from its report (i.e. corn) as the indirect emissions from converting unsustainable feedstock into fuel largely offset the environmental benefit ( i.e. lower direct emissions). The Renewable Fuels Feedstock Conundrum 5 960 320 580 660 1,100 70 85 40 Municipal solid waste Wood-processing waste Forestry residues Agricultural residues Cellulosic cover crops Oil-cover crops Oil trees on degraded land Waste and residue lipids Proven Technologies Advanced Technologies ▪ The finite amount of sustainable feedstock constrains the production of renewable fuels ▪ Producers need to choose between pursuing abundant feedstocks or proven technologies ‒ Abundant feedstocks require advanced technologies ‒ Proven technologies use competitive feedstocks ▪ GCEH aims to solve the issue with our proprietary Camelina feedstock and proven technology Used cooking oil (industrial or private sources) Animal waste fat (tallow) Other (i.e. tall oil, technical corn oil, fish oil, POME, PFAD) Jatropha, p ongamia Camelina , carinata, pennycress Miscanthus, switchgrass, reed cannarygrass Rice straw, sugar cane bagasse, other (i.e. corn stover, cereal residues) Left overs from logging operations (i.e. leaves, lops, tops, damaged or unwanted stem wood) By - products and co - products of industrial wood - processing operations (i.e. sawmill slabs, saw dust, wood chip) May contain up to 20% non - reusable plastics; typically inefficient to separate organics and plastic

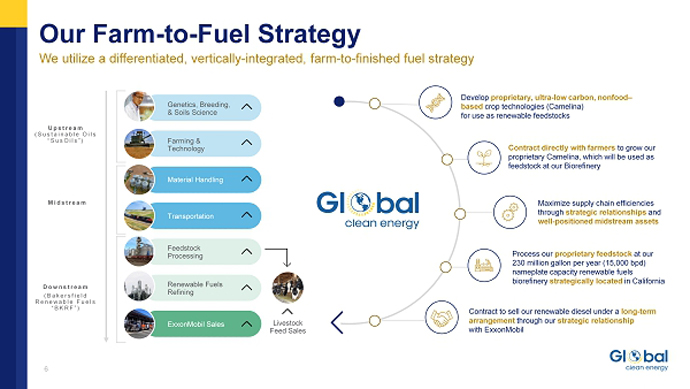

Genetics, Breeding, & Soils Science Farming & Technology Material Handling Transportation Feedstock Processing Renewable Fuels Refining ExxonMobil Sales Upstream (Sustainable Oils “SusOils”) Midstream Downstream (Bakersfield Renewable Fuels “BKRF”) Livestock Feed Sales Develop proprietary, ultra - low carbon, nonfood – based crop technologies (Camelina) for use as renewable feedstocks Process our proprietary feedstock at our 230 million gallon per year (15,000 bpd) nameplate capacity renewable fuels biorefinery strategically located in California Maximize supply chain efficiencies through strategic relationships and well - positioned midstream assets Contract directly with farmers to grow our proprietary Camelina, which will be used as feedstock at our Biorefinery Contract to sell our renewable diesel under a long - term arrangement through our strategic relationship with ExxonMobil Our Farm - to - Fuel Strategy We utilize a differentiated, vertically - integrated, farm - to - finished fuel strategy 6

Investment Highlights

1 Vertically - Integrated, Sustainable, Scalable, “Farm - to - Fuel” Solution 2 Ample Access to Reliable Feedstock for BKRF 3 Long - Term Offtake Agreement with ExxonMobil Provides Margin Certainty 4 Ultra - Low Carbon Intensity (“CI”) Score Drives Higher RD Value 5 Proprietary Feedstock with Leading Value Proposition 6 Strategically Located Biorefinery with Early Entrant Advantage 7 Favorable Industry Trends and Regulatory Environment Supports Long - Term RD Growth Investment Highlights 8

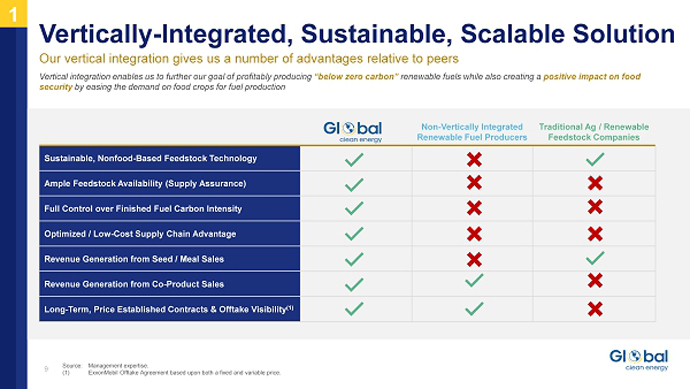

Vertical integration enables us to further our goal of profitably producing “below zero carbon” renewable fuels while also creating a positive impact on food security by easing the demand on food crops for fuel production Non - Vertically Integrated Renewable Fuel Producers Traditional Ag / Renewable Feedstock C ompanies Sustainable, Nonfood - Based Feedstock Technology Ample Feedstock Availability (Supply Assurance) Full Control over Finished Fuel Carbon Intensity Optimized / Low - Cost Supply Chain Advantage Revenue Generation from Seed / Meal Sales Revenue Generation from Co - Product Sales Long - Term , Price Established Contracts & Offtake Visibility (1) Vertically - Integrated, Sustainable, Scalable Solution Our vertical integration gives us a number of advantages relative to peers 9 1 Source: Management expertise. (1) ExxonMobil Offtake Agreement based upon both a fixed and variable price.

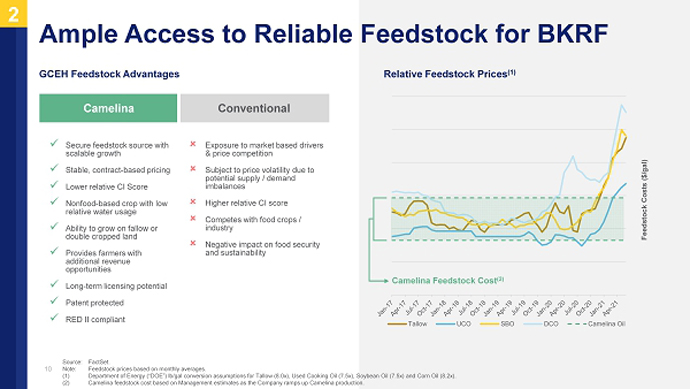

Feedstock Costs ($/gal) Tallow UCO SBO DCO Camelina Oil Relative Feedstock Prices (1) Camelina Conventional x Secure feedstock source with scalable growth x Stable, contract - based pricing x Lower relative CI Score x Nonfood - based crop with low relative water usage x Ability to grow on fallow or double cropped land x Provides farmers with additional revenue opportunities x Long - term licensing potential x Patent protected x RED II compliant Exposure to market based drivers & price competition Subject to price volatility due to potential supply / demand imbalances Higher relative CI score Competes with food crops / industry Negative impact on food security and sustainability Ample Access to Reliable Feedstock for BKRF GCEH Feedstock Advantages 10 2 Source: FactSet. Note: Feedstock prices based on monthly averages. (1) Department of Energy (“DOE”) lb/gal conversion assumptions for Tallow (8.0x), Used Cooking Oil (7.5x), Soybean Oil (7.5x) and Corn Oil (8.2x). (2) Camelina feedstock cost based on Management estimates as the Company ramps up Camelina production. Camelina Feedstock Cost (2 )

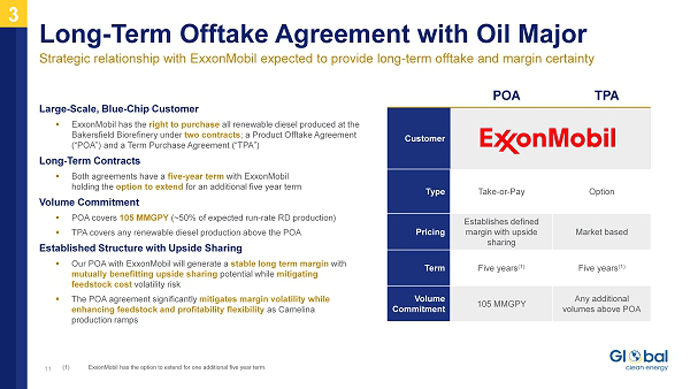

Large - Scale , Blue - Chip Customer ▪ ExxonMobil has the right to purchase all renewable diesel produced at the Bakersfield Biorefinery under two contracts ; a Product Offtake Agreement (“POA ”) and a Term Purchase Agreement (“TPA”) Long - Term Contracts ▪ Both agreements have a five - year term with ExxonMobil holding the option to extend for an additional five year term Volume Commitment ▪ POA covers 105 MMGPY (~50% of expected run - rate RD production) ▪ TPA covers any renewable diesel production above the POA Established Structure with Upside Sharing ▪ Our POA with ExxonMobil will generate a stable long term margin with mutually benefitting upside sharing potential while mitigating feedstock cost volatility risk ▪ The POA agreement significantly mitigates margin volatility while enhancing feedstock and profitability flexibility as Camelina production ramps POA TPA Customer Type Take - or - Pay Option Pricing Establishes defined margin with upside sharing Market based Term Five years (1) Five years (1) Volume Commitment 105 MMGPY Any additional volumes above POA Long - Term Offtake Agreement with Oil Major Strategic relationship with ExxonMobil expected to provide long - term offtake and margin certainty 11 3 ( 1) ExxonMobil has the option to extend for one additional five year term.

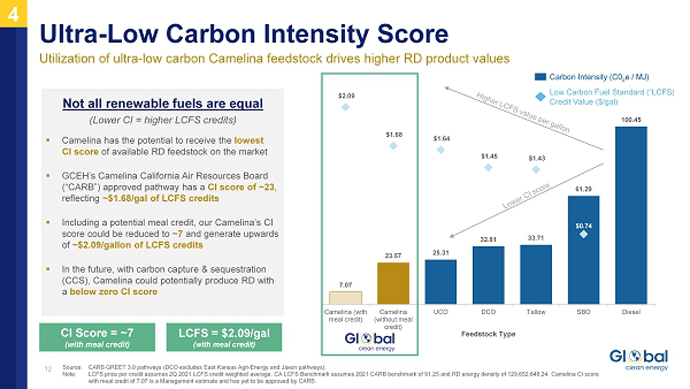

7.07 23.57 25.31 32.81 33.71 61.29 100.45 $2.09 $1.68 $1.64 $1.45 $1.43 $0.74 $- $0.50 $1.00 $1.50 $2.00 0 20 40 60 80 100 120 Camelina (with meal credit) Camelina (without meal credit) UCO DCO Tallow SBO Diesel Feedstock Type Not all renewable fuels are equal (Lower CI = higher LCFS credits) ▪ Camelina has the potential to receive the lowest CI score of available RD feedstock on the market ▪ GCEH’s Camelina California Air Resources Board (“CARB”) approved pathway has a CI score of ~ 23 , reflecting ~$ 1.68/gal of LCFS credits ▪ Including a potential meal credit, our Camelina’s CI score could be reduced to ~7 and generate upwards of ~$ 2.09/gallon of LCFS credits ▪ In the future, with carbon capture & sequestration (CCS), Camelina could potentially produce RD with a below zero CI score CI Score = ~7 (with meal credit) LCFS = $ 2.09/gal (with meal credit) Low Carbon Fuel Standard (“LCFS) Credit Value ($/gal) Carbon Intensity (C0 2 e / MJ) Ultra - Low Carbon Intensity Score Utilization of ultra - low carbon Camelina feedstock drives higher RD product values 12 4 Source: CARB GREET 3.0 pathways (DCO excludes East Kansas Agri - Energy and Jaxon pathways). Note: LCFS price per credit assumes 2Q 2021 LCFS credit weighted average, CA LCFS Benchmark assumes 2021 CARB benchmark of 91.25 and RD energy density of 129,652,648.24. Camelina CI score with meal credit of 7.07 is a Management estimate and has yet to be approved by CARB.

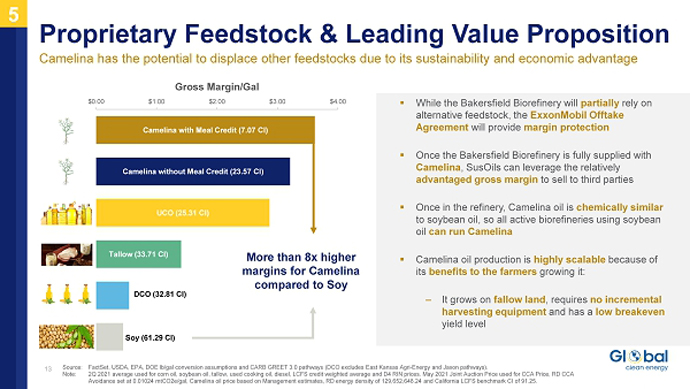

Camelina with Meal Credit (7.07 CI) Camelina without Meal Credit (23.57 CI) UCO (25.31 CI) Tallow (33.71 CI) DCO (32.81 CI) Soy (61.29 CI) $0.00 $1.00 $2.00 $3.00 $4.00 Gross Margin/Gal Proprietary Feedstock & Leading Value Proposition Camelina has the potential to displace other feedstocks due to its sustainability and economic advantage 13 5 ▪ While the Bakersfield Biorefinery will partially rely on alternative feedstock, the ExxonMobil Offtake Agreement will provide margin protection ▪ Once the Bakersfield Biorefinery is fully supplied with Camelina , SusOils can leverage the relatively advantaged gross margin to sell to third parties ▪ Once in the refinery, Camelina oil is chemically similar to soybean oil, so all active biorefineries using soybean oil can run Camelina ▪ Camelina oil production is highly scalable because of its benefits to the farmers growing it: ‒ It grows on fallow land , requires no incremental harvesting equipment and has a low breakeven yield level Source: FactSet, USDA, EPA, DOE lb/gal conversion assumptions and CARB GREET 3.0 pathways (DCO excludes East Kansas Agri - Energy and Jaxon pathways ). Note: 2Q 2021 average used for corn oil, soybean oil, tallow, used cooking oil, diesel, LCFS credit weighted average and D4 RIN prices. May 2021 Joint Auction Price used for CCA Price, RD CCA Avoidance set at 0.01024 mtCO2e/gal, Camelina oil price based on Management estimates, RD energy density of 129,652,648.24 and California LCFS benchmark CI of 91.25. More than 8 x higher margins for Camelina compared to Soy

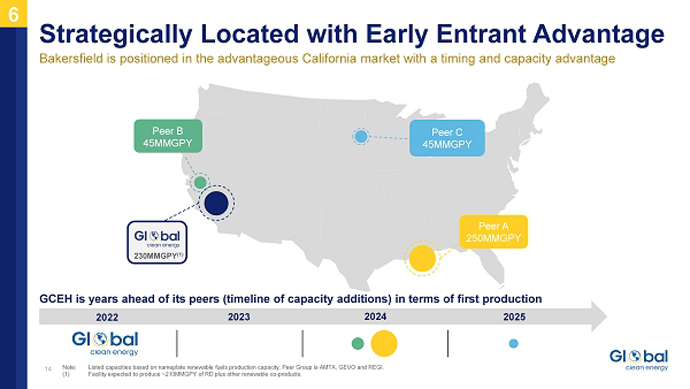

Peer B 45MMGPY Peer C 45MMGPY Peer A 250MMGPY GCEH is years ahead of its peers (timeline of capacity additions ) in terms of first production 2022 2023 2024 2025 230MMGPY (1) Strategically Located with Early Entrant Advantage Bakersfield is positioned in the advantageous California market with a timing and capacity advantage 14 6 Note: Listed capacities based on nameplate renewable fuels production capacity. Peer Group is AMTX, GEVO and REGI. (1) Facility expected to produce ~210MMGPY of RD plus other renewable co - products.

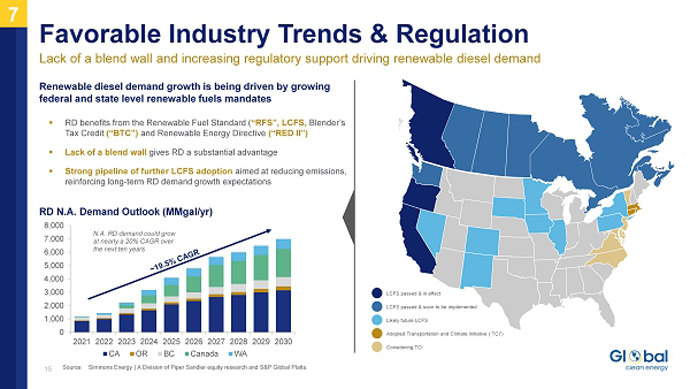

Renewable diesel demand growth is being driven by growing federal and state level renewable fuels mandates ▪ RD benefits from the Renewable Fuel Standard ( “RFS”, LCFS, Blender’s Tax Credit (“BTC”) and Renewable Energy Directive (“RED II”) ▪ Lack of a blend wall gives RD a substantial advantage ▪ Strong pipeline of further LCFS adoption aimed at reducing emissions, reinforcing long - term RD demand growth expectations RD N.A. Demand Outlook (MMgal/yr) 0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 CA OR BC Canada WA N.A. RD demand could grow at nearly a 20% CAGR over the next ten years Favorable Industry Trends & Regulation Lack of a blend wall and increasing regulatory support driving renewable diesel demand 15 7 Source: Simmons Energy | A Division of Piper Sandler equity research and S&P Global Platts. LCFS passed & in effect Likely future LCFS LCFS passed & soon to be implemented Adopted Transportation and Climate Initiative (“TCI”) Considering TCI

Business Overview

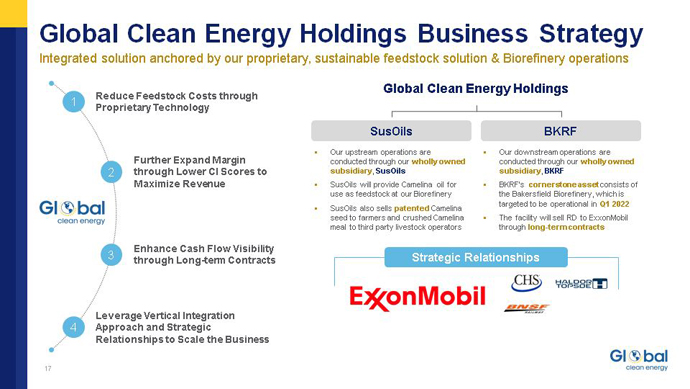

Reduce Feedstock Costs through Proprietary Technology Further Expand Margin through Lower CI Scores to Maximize Revenue Enhance Cash Flow Visibility through Long - term Contracts Leverage Vertical Integration Approach and Strategic Relationships to Scale the Business 1 2 3 4 ▪ Our upstream operations are conducted through our wholly owned subsidiary , SusOils ▪ SusOils will provide Camelina oil for use as feedstock at our Biorefinery ▪ SusOils also sells patented Camelina seed to farmers and crushed Camelina meal to third party livestock operators SusOils BKRF ▪ Our downstream operations are conducted through our wholly owned subsidiary , BKRF ▪ BKRF’s cornerstone asset consists of the Bakersfield Biorefinery, which is targeted to be operational in Q1 2022 ▪ The facility will sell RD to ExxonMobil through long - term contracts Global Clean Energy Holdings Strategic Relationships Global Clean Energy Holdings Business Strategy Integrated solution anchored by our proprietary, sustainable feedstock solution & Biorefinery operations 17

We have identified nearly 50 million target acres for potential Camelina cultivation across eight states We currently have substantial acreage under commercial cultivation across six states Average Acreage Owned per Operator = >6,000 CA WA MT ID OR WY CO KS OK State # of Farming Operations Target Acres Washington 1,700 5.5MM Montana 1,300 15MM Oregon 410 1.5MM Idaho 60 300K Wyoming 20 400K Colorado 900 5.5MM Kansas 2,800 11.3MM Oklahoma 2,100 7.6MM Camelina Cultivation Strategy Camelina Grower Pipeline 14 Years of Plant Science / R&D Work States with planned commercial cultivation of our proprietary Camelina Biorefinery States currently with commercial cultivation of our proprietary Camelina Contract with farmers to grow Camelina grain that will be processed into oil for use in Bakersfield Biorefinery Pay farmers on a per pound of harvested grain basis Distribute certified Camelina grower seed to farmers through strong relationship with CHS Inc., an agribusiness cooperative owned by farmers Farmers plant the seeds using fertilizers, chemicals and other supplies through grower cooperatives Upstream Operations We will contract directly with growers / farmers to cultivate, grow and produce our proprietary Camelina 18 Source: Management estimates.

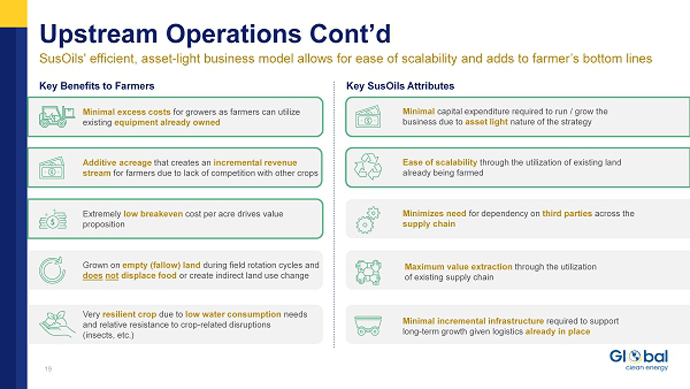

Key Benefits to Farmers Key SusOils Attributes Minimal capital expenditure required to run / grow the business due to asset light nature of the strategy Ease of scalability through the utilization of existing land already being farmed Minimal incremental infrastructure required to support long - term growth given logistics already in place Minimizes need for dependency on third parties across the supply chain Maximum value extraction through the utilization of existing supply chain Minimal excess costs for growers as farmers can utilize existing equipment already owned Additive acreage that creates an incremental revenue stream for farmers due to lack of competition with other crops Grown on empty (fallow) land during field rotation cycles and does not displace food or create indirect land use change Extremely low breakeven cost per acre drives value proposition Very resilient crop due to low water consumption needs and relative resistance to crop - related disruptions ( insects, etc.) Upstream Operations Cont’d SusOils ' efficient, asset - light business model allows for ease of scalability and adds to farmer’s bottom lines 19

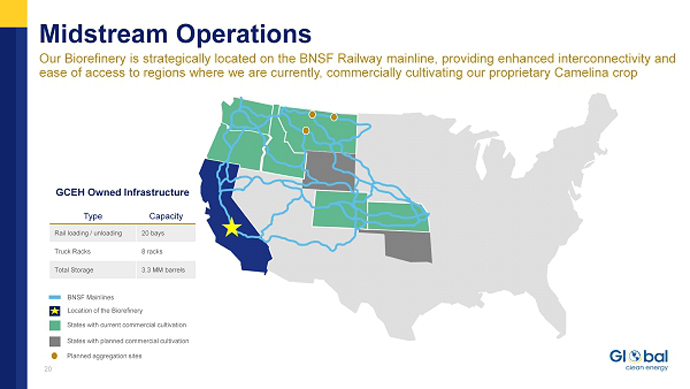

States with current commercial cultivation States with planned commercial cultivation Location of the Biorefinery BNSF Mainlines Midstream Operations Our Biorefinery is strategically located on the BNSF Railway mainline , providing enhanced interconnectivity and ease of access to regions where we are currently, commercially cultivating our proprietary Camelina crop 20 GCEH Owned Infrastructure Type Capacity Rail loading / unloading 20 bays Truck Racks 8 racks Total Storage 3 .3 MM barrels Planned aggregation sites

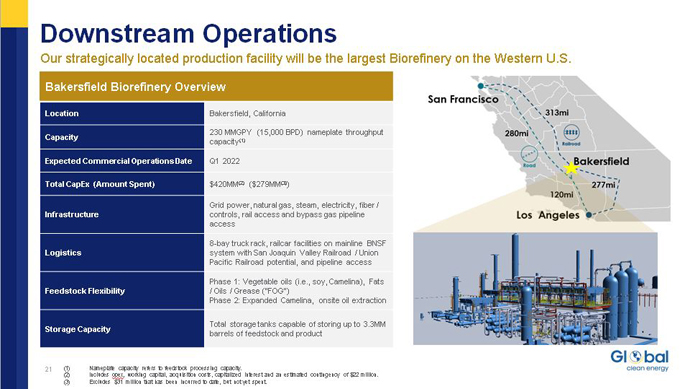

Bakersfield Biorefinery Overview Location Bakersfield, California Capacity 230 MMGPY (15,000 BPD) nameplate throughput capacity (1) Expected Commercial Operations Date Q1 2022 Total CapEx ( Amount Spent ) $420MM (2) ($279MM (3) ) Infrastructure Grid power, natural gas, steam, electricity, fiber / controls , rail access and bypass gas pipeline access Logistics 8 - bay truck rack, railcar facilities o n mainline BNSF system with San Joaquin Valley Railroad / Union Pacific Railroad potential, and pipeline access Feedstock Flexibility Phase 1: Vegetable oils (i.e., soy , Camelina), Fats / Oils / Grease (“FOG”) Phase 2: E xpanded Camelina, onsite oil extraction Storage Capacity Total storage tanks capable of storing up to 3.3MM barrels of feedstock and product Downstream Operations Our strategically located production facility will be the largest Biorefinery on the Western U.S. 21 (1) Nameplate capacity refers to feedstock processing capacity. (2) Includes opex, working capital, acquisition costs, capitalized interest and an estimated contingency of $22 million. (3) Excludes $31 million that has been incurred to date, but not yet spent.

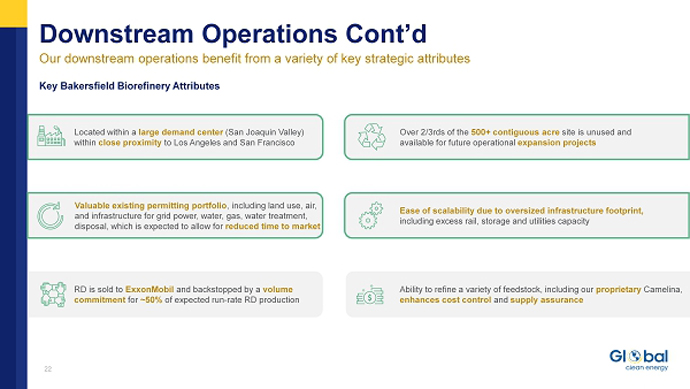

Downstream Operations Cont’d Our downstream operations benefit from a variety of key strategic attributes 22 Key Bakersfield Biorefinery Attributes Located within a large demand center (San Joaquin Valley) within close proximity to Los Angeles and San Francisco Ability to refine a variety of feedstock, including our proprietary Camelina, enhances cost control and supply assurance Valuable existing permitting portfolio , including land use, air, and infrastructure for grid power, water, gas, water treatment, disposal, which is expected to allow for reduced time to market Over 2/3rds of the 500 + contiguous acre site is unused and available for future operational expansion projects Ease of scalability due to oversized infrastructure footprint, including excess rail, storage and utilities capacity RD is sold to ExxonMobil and backstopped by a volume commitment for ~50% of expected run - rate RD production

• Solution to hydrogen capacity constraint on RD production, production from 150 to 210 MMGPY • More efficient Steam Methane Reforming, reducing the CI of output and lower natural gas costs • Surplus H2 to market or to further expansion of the Biorefinery Hydrogen Plant Expansion Midstream Agriculture Assets • Grain elevation, cleaning and storage assets located near primary Camelina agricultural regions • Focus on Northern Plains, Pacific Northwest and Midwest Onsite Crush Plant • Crush Camelina and soybeans onsite, removing the need to pay for toll - processing • Benefits: feedstock cost, lower CI , waste stream utilization, meal sales, corporate credits and supply certainty Carbon Capture • Capture 65% to greater than 95% of CO2 sequestration and synthetic fuels production • Permit case complete, pending submission to SJV Air District • Potential to benefit from Section 45(Q) tax credit for carbon sequestration Biorefinery Expansion • Total estimated cost of $250MM (1) • Increases capacity by an additional 15,000+ BPD Waste Heat Recovery to Power • Use waste heat to generate electricity and steam for the facility Solar PV • Displace grid energy with solar electricity produced onsite • Accelerate Camelina development • Grow local and regional feedstock relationships • Expand purpose grown Camelina to greater overall percentage of feed demand Camelina Development Bakersfield Biorefinery • Target online date in Q1 2022 • Continue managing Engineering, Procurement & Construction (“EPC”) process to begin RD output and delivery Phase II Growth Current Development Phase III Growth Strategy to Long - term Sustainability Growth Strategy Global Clean is pursuing multiple strategic avenues to long - term growth 23 (1) CapEx projections are included herein for illustrative purposes only; actual expenditures are likely to vary.

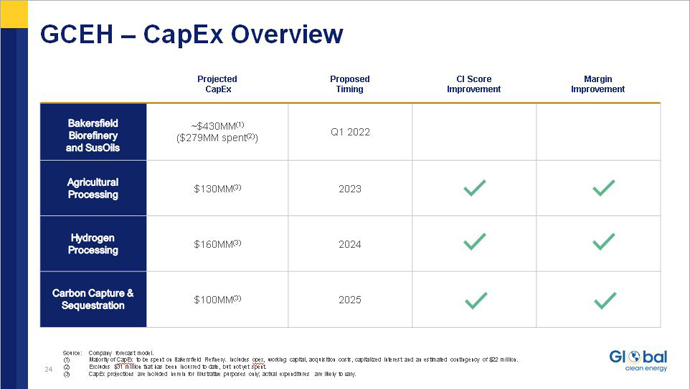

GCEH – CapEx Overview 24 Projected CapEx Proposed Timing CI Score Improvement Margin Improvement ~$430MM (1) ($279MM spent (2) ) Q1 2022 $ 130 MM (3) 2023 $ 160MM (3) 2024 $100MM (3) 2025 Source: Company forecast model. (1) Majority of CapEx to be spent on Bakersfield Refinery. Includes opex, working capital, acquisition costs, capitalized interest and an estimated contingency of $22 million. (2) Excludes $31 million that has been incurred to date, but not yet spent. (3) CapEx projections are included herein for illustrative purposes only; actual expenditures are likely to vary.

Appendix

Independent Audit Committee Compensation Committee Governance Committee Martin Wenzel Director David Walker Independent Director SLAE Inc. Phyllis Currie Independent Director Susan Anhalt Independent Director Richard Palmer CEO, President & Founder Prior Experience Education Board of Directors Overview 26

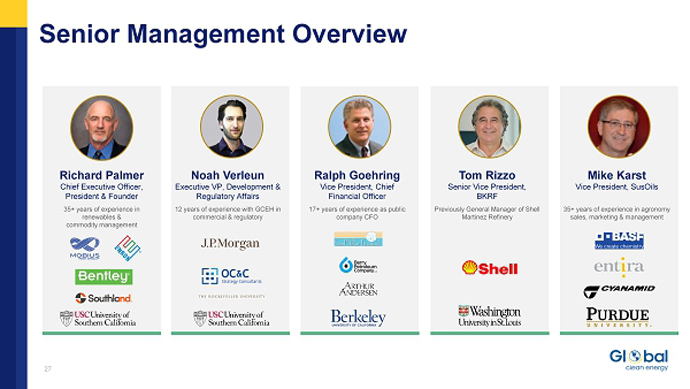

Richard Palmer Chief Executive Officer, President & Founder 35+ years of experience in renewables & commodity management Senior Management Overview 27 Mike Karst Vice President, SusOils 35+ years of experience in agronomy sales, marketing & management Tom Rizzo Senior Vice President, BKRF Previously General Manager of Shell Martinez Refinery Ralph Goehring Vice President, Chief Financial Officer 17+ years of experience as public company CFO Noah Verleun Executive VP, Development & Regulatory Affairs 12 years of experience with GCEH in commercial & regulatory

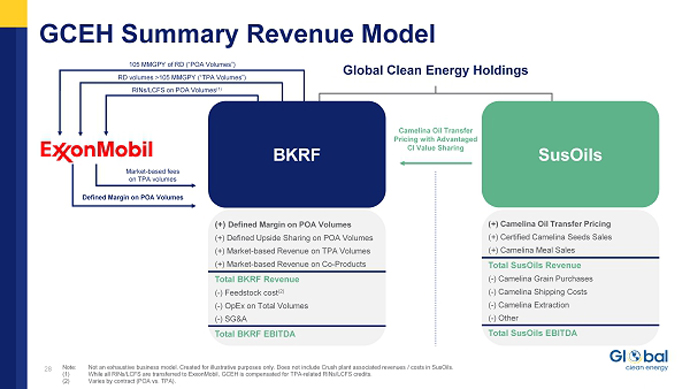

28 GCEH Summary Revenue Model Note: Not an exhaustive business model. Created for illustrative purposes only. Does not include Crush plant associated revenues / costs in SusOils. (1) While all RINs/LCFS are transferred to ExxonMobil, GCEH is compensated for TPA - related RINs/LCFS credits. (2 ) Varies by contract (POA vs. TPA ). RINs/LCFS on POA Volumes (1) 105 MMGPY of RD (“POA Volumes”) RD volumes >105 MMGPY (“TPA Volumes”) Defined Margin on POA Volumes (+) Defined Margin on POA Volumes (+) Defined Upside Sharing on POA Volumes (+) Market - based Revenue on TPA Volumes (+) Market - based Revenue on Co - Products Total BKRF Revenue ( - ) Feedstock cost (2) ( - ) OpEx on Total Volumes ( - ) SG&A Total BKRF EBITDA (+) Camelina Oil Transfer Pricing (+) Certified Camelina Seeds Sales (+) Camelina Meal Sales Total SusOils Revenue ( - ) Camelina Grain Purchases ( - ) Camelina Shipping Costs ( - ) Camelina Extraction ( - ) Other Total SusOils EBITDA Camelina Oil Transfer Pricing with Advantaged CI Value Sharing Market - based fees on TPA volumes Global Clean Energy Holdings SusOils BKRF

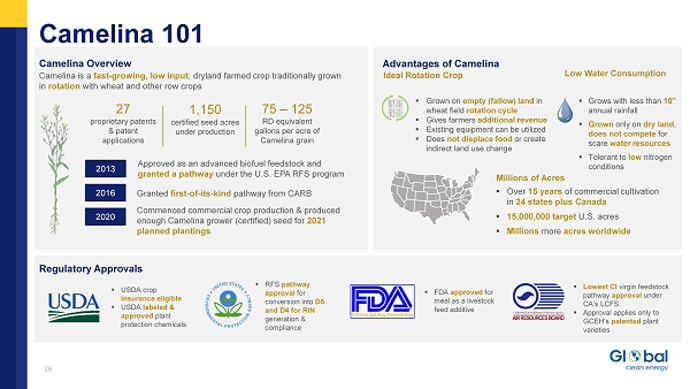

Ideal Rotation Crop Low Water Consumption Millions of Acres ▪ Grown on empty (fallow) land in wheat field rotation cycle ▪ Gives farmers additional revenue ▪ Existing equipment can be utilized ▪ Does not displace food or create indirect land use change ▪ Grows with less than 10” annual rainfall ▪ Grown only on dry land , does not compete for scare water resources ▪ Tolerant to low nitrogen conditions ▪ Over 15 years of commercial cultivation in 24 states plus Canada ▪ 15,000,000 target U.S. acres ▪ Millions more acres worldwide 2013 Approved as an advanced biofuel feedstock and granted a pathway under the U.S. EPA RFS program 2016 Granted first - of - its - kind pathway from CARB 2020 Commenced commercial crop production & produced enough Camelina grower (certified) seed for 2021 planned plantings Camelina is a fast - growing, low input , dryland farmed crop traditionally grown in rotation with wheat and other row crops 27 proprietary patents & patent applications 1,150 certified seed acres under production 75 – 125 RD equivalent gallons per acre of Camelina grain ▪ USDA crop insurance eligible ▪ USDA labeled & approved plant protection chemicals ▪ RFS pathway approval for conversion into D5 and D4 for RIN generation & compliance ▪ FDA approved for meal as a livestock feed additive ▪ Lowest CI virgin feedstock pathway approval under CA’s LCFS ▪ Approval applies only to GCEH’s patented plant varieties Camelina Overview Advantages of Camelina Regulatory Approvals Camelina 101 29

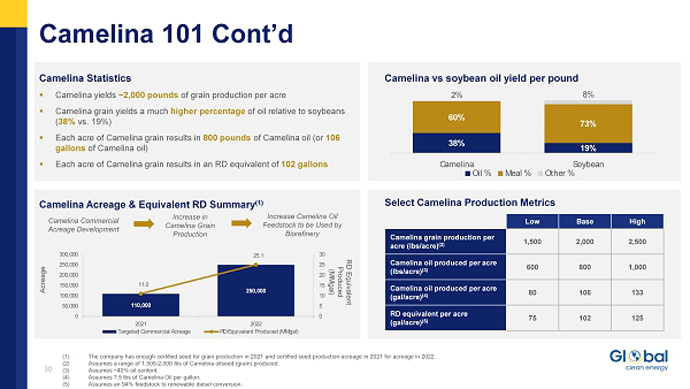

▪ Camelina yields ~2,000 pounds of grain production per acre ▪ Camelina grain yields a much higher percentage of oil relative to soybeans ( 38% vs. 19%) ▪ Each acre of Camelina grain results in 800 pounds of Camelina oil (or 106 gallons of Camelina oil) ▪ Each acre of Camelina grain results in an RD equivalent of 102 gallons Camelina Commercial Acreage Development Increase in Camelina Grain Production Increase Camelina Oil F eedstock to be Used by Biorefinery 38% 19% 60% 73% 2% 8% Camelina Soybean Oil % Meal % Other % 110,000 250,000 11.0 25.1 0 5 10 15 20 25 30 0 50,000 100,000 150,000 200,000 250,000 300,000 2021 2022 Targeted Commercial Acreage RD Equivalent Produced (MMgal) Acreage RD Equivalent Produced (MMgal) Low Base High Camelina grain production per acre (lbs/acre ) (2) 1,500 2,000 2,500 Camelina oil produced per acre (lbs/acre ) (3) 600 800 1,000 Camelina oil produced per acre (gal/acre ) (4) 80 106 133 RD equivalent per acre (gal/acre ) (5) 75 102 125 Camelina Statistics Camelina vs soybean oil yield per pound Camelina Acreage & Equivalent RD Summary (1) Select Camelina Production Metrics Camelina 101 Cont’d 30 (1) The company has enough c ertified seed for grain production in 2021 and certified seed production acreage in 2021 for acreage in 2022. (2) Assumes a range of 1,500 - 2,000 lbs of Camelina oilseed (grain) produced. (3) Assumes ~40% oil content. (4) Assumes 7.5 lbs of Camelina Oil per gallon. (5) Assumes an 94% feedstock to renewable diesel conversion.

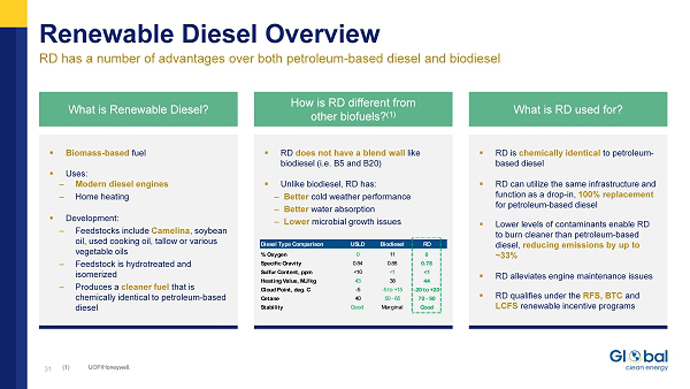

▪ RD is chemically identical to petroleum - based diesel ▪ RD can utilize the same infrastructure and function as a drop - in, 100% replacement for petroleum - based diesel ▪ Lower levels of contaminants enable RD to burn cleaner than petroleum - based diesel, reducing emissions by up to ~33% ▪ RD alleviates engine maintenance issues ▪ RD qualifies under the RFS, BTC and LCFS renewable incentive programs What is RD used for? ▪ Biomass - based fuel ▪ Uses: ‒ Modern diesel engines ‒ Home heating ▪ Development: ‒ Feedstocks include Camelina , soybean oil, used cooking oil, tallow or various vegetable oils ‒ Feedstock is hydrotreated and isomerized ‒ Produces a cleaner fuel that is chemically identical to petroleum - based diesel What is Renewable Diesel? ▪ RD does not have a blend wall like biodiesel ( i.e. B5 and B20) ▪ Unlike biodiesel, RD has: ‒ Better cold weather performance ‒ Better water absorption ‒ Lower microbial growth issues How is RD different from other biofuels? (1) Diesel Type Comparison USLD Biodiesel RD % Oxygen 0 11 0 Specific Gravity 0.84 0.88 0.78 Sulfur Content, ppm <10 <1 <1 Heating Value, MJ/kg 43 38 44 Cloud Point, deg. C -5 -5 to +15 -20 to +20 Cetane 40 50 - 65 70 - 90 Stability Good Marginal Good Renewable Diesel Overview RD has a number of advantages over both petroleum - based diesel and biodiesel 31 ( 1) UOP/Honeywell.

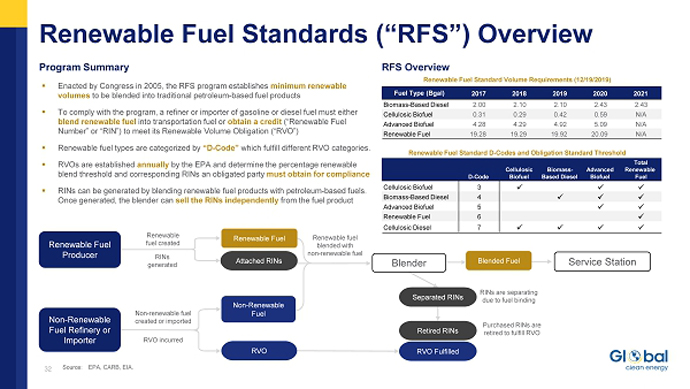

Program Summary 32 ▪ Enacted by Congress in 2005, the RFS program establishes minimum renewable volumes to be blended into traditional petroleum - based fuel products ▪ To comply with the program, a refiner or importer of gasoline or diesel fuel must either blend renewable fuel into transportation fuel or obtain a credit (“Renewable Fuel Number” or “RIN”) to meet its Renewable Volume Obligation (“RVO”) ▪ Renewable fuel types are categorized by “D - Code” which fulfill different RVO categories. ▪ RVOs are established annually by the EPA and determine the percentage renewable blend threshold and corresponding RINs an obligated party must obtain for compliance ▪ RINs can be generated by blending renewable fuel products with petroleum - based fuels. Once generated, the blender can sell the RINs independently from the fuel product Renewable fuel created RINs generated Renewable fuel blended with non - renewable fuel Non - renewable fuel created or imported RVO incurred RINs are separating due to fuel binding Purchased RINs are retired to fulfill RVO Renewable Fuel Standard Volume Requirements (12/19/2019) Fuel Type (Bgal) 2017 2018 2019 2020 2021 Biomass - Based Diesel 2.00 2.10 2.10 2.43 2.43 Cellulosic Biofuel 0.31 0.29 0.42 0.59 N/A Advanced Biofuel 4.28 4.29 4.92 5.09 N/A Renewable Fuel 19.28 19.29 19.92 20.09 N/A Renewable Fuel Standard D - Codes and Obligation Standard Threshold Total Cellulosic Biomass - Advanced Renewable D - Code Biofuel Based Diesel Biofuel Fuel Cellulosic Biofuel 3 x x x Biomass - Based Diesel 4 x x x Advanced Biofuel 5 x x Renewable Fuel 6 x Cellulosic Diesel 7 x x x x RFS Overview Renewable Fuel Standards (“RFS”) Overview 32 Source: EPA, CARB, EIA. RVO Non - Renewable Fuel Attached RINs Renewable Fuel Renewable Fuel Producer Non - Renewable Fuel Refinery or Importer RVO Fulfilled Retired RINs Separated RINs Blender Blended Fuel Service Station

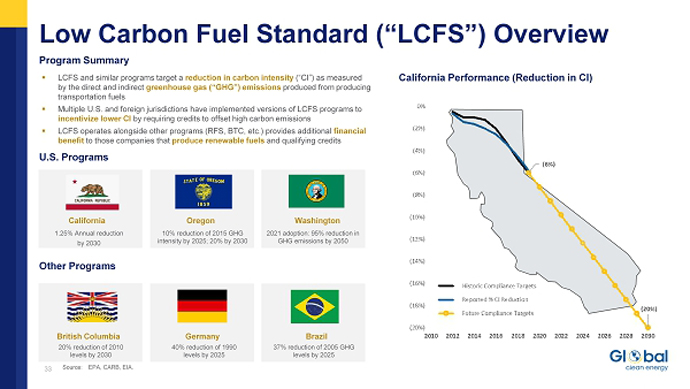

▪ LCFS and similar programs target a reduction in carbon intensity (“CI”) as measured by the direct and indirect greenhouse gas (“GHG”) emissions produced from producing transportation fuels ▪ Multiple U.S. and foreign jurisdictions have implemented versions of LCFS programs to incentivize lower CI by requiring credits to offset high carbon emissions ▪ LCFS operates alongside other programs (RFS, BTC, etc.) provides additional financial benefit to those companies that produce renewable fuels and qualifying credits California Oregon Washington 1.25% Annual reduction by 2030 10% reduction of 2015 GHG intensity by 2025; 20% by 2030 2021 adoption: 95% reduction in GHG emissions by 2050 British Columbia 20% reduction of 2010 levels by 2030 Germany 40% reduction of 1990 levels by 2025 Brazil 37% reduction of 2005 GHG levels by 2025 Program Summary California Performance (Reduction in CI) U.S. Programs Other Programs Low Carbon Fuel Standard (“LCFS”) Overview 33 Source: EPA, CARB, EIA.

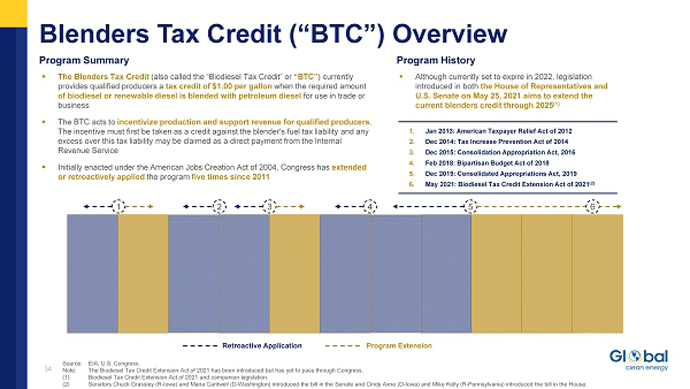

Program Summary ▪ The Blenders Tax Credit (also called the “Biodiesel Tax Credit” or “BTC” ) currently provides qualified producers a tax credit of $1.00 per gallon when the required amount of biodiesel or renewable diesel is blended with petroleum diesel for use in trade or business ▪ The BTC acts to incentivize production and support revenue for qualified producers . The incentive must first be taken as a credit against the blender's fuel tax liability and any excess over this tax liability may be claimed as a direct payment from the Internal Revenue Service ▪ Initially enacted under the American Jobs Creation Act of 2004, Congress has extended or retroactively applied the program five times since 2011 ▪ Although currently set to expire in 2022, legislation introduced in both the House of Representatives and U.S. Senate on May 25, 2021 aims to extend the current blenders credit through 2025 (1) Program History 1. Jan 2013: American Taxpayer Relief Act of 2012 2. Dec 2014: Tax Increase Prevention Act of 2014 3. Dec 2015: Consolidation Appropriation Act, 2016 4. Feb 2018: Bipartisan Budget Act of 2018 5. Dec 2019: Consolidated Appropriations Act, 2019 6. May 2021: Biodiesel Tax Credit Extension Act of 2021 (2) 1 2 3 4 5 Retroactive Application Program Extension Blenders Tax Credit (“BTC ”) Overview 34 Source: EIA, U.S. Congress. Note: The Biodiesel Tax Credit Extension Act of 2021 has been introduced but has yet to pass through Congress. (1) Biodiesel Tax Credit Extension Act of 2021 and companion legislation . (2) Senators Chuck Grassley (R - Iowa) and Maria Cantwell (D - Washington) introduced the bill in the Senate and Cindy Axne (D - Iowa) and Mike Kelly (R - Pennsylvania) introduced the bill in the House. 6

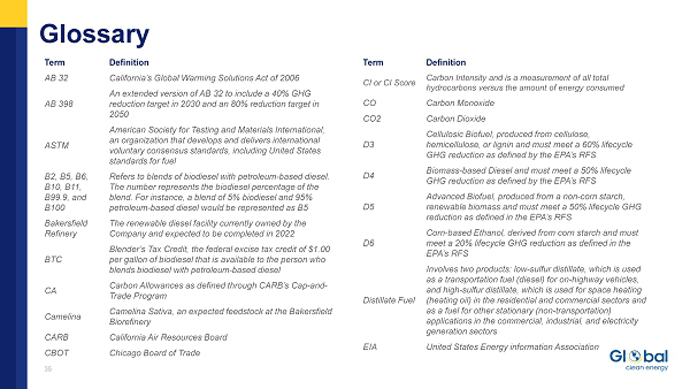

Glossary 35 Term Definition AB 32 California’s Global Warming Solutions Act of 2006 AB 398 An extended version of AB 32 to include a 40% GHG reduction target in 2030 and an 80% reduction target in 2050 ASTM American Society for Testing and Materials International, an organization that develops and delivers international voluntary consensus standards, including United States standards for fuel B2, B5, B6, B10, B11, B99.9, and B100 Refers to blends of biodiesel with petroleum - based diesel. The number represents the biodiesel percentage of the blend. For instance, a blend of 5% biodiesel and 95% petroleum - based diesel would be represented as B5 Bakersfield Refinery The renewable diesel facility currently owned by the Company and expected to be completed in 2022 BTC Blender’s Tax Credit, the federal excise tax credit of $1.00 per gallon of biodiesel that is available to the person who blends biodiesel with petroleum - based diesel CA Carbon Allowances as defined through CARB’s Cap - and - Trade Program Camelina Camelina Sativa, an expected feedstock at the Bakersfield Biorefinery CARB California Air Resources Board CBOT Chicago Board of Trade Term Definition CI or CI Score Carbon Intensity and is a measurement of all total hydrocarbons versus the amount of energy consumed CO Carbon Monoxide CO2 Carbon Dioxide D3 Cellulosic Biofuel, produced from cellulose, hemicellulose, or lignin and must meet a 60% lifecycle GHG reduction as defined by the EPA’s RFS D4 Biomass - based Diesel and must meet a 50% lifecycle GHG reduction as defined by the EPA’s RFS D5 Advanced Biofuel, produced from a non - corn starch, renewable biomass and must meet a 50% lifecycle GHG reduction as defined in the EPA’s RFS D6 Corn - based Ethanol, derived from corn starch and must meet a 20% lifecycle GHG reduction as defined in the EPA’s RFS Distillate Fuel Involves two products: low - sulfur distillate, which is used as a transportation fuel (diesel) for on - highway vehicles, and high - sulfur distillate, which is used for space heating (heating oil) in the residential and commercial sectors and as a fuel for other stationary (non - transportation) applications in the commercial, industrial, and electricity generation sectors EIA United States Energy information Association

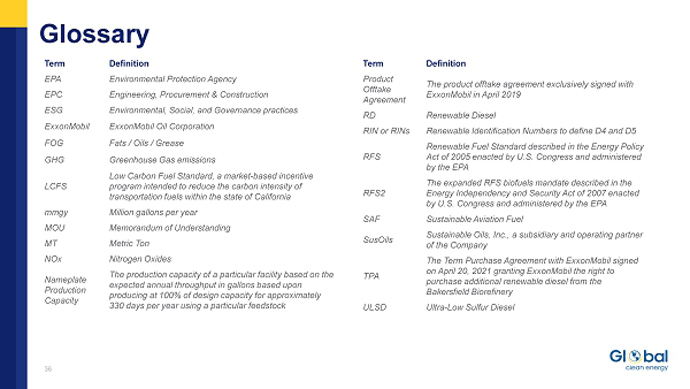

Glossary 36 Term Definition EPA Environmental Protection Agency EPC Engineering, Procurement & Construction ESG Environmental, Social, and Governance practices ExxonMobil ExxonMobil Oil Corporation FOG Fats / Oils / Grease GHG Greenhouse Gas emissions LCFS Low Carbon Fuel Standard, a market - based incentive program intended to reduce the carbon intensity of transportation fuels within the state of California mmgy Million gallons per year MOU Memorandum of Understanding MT Metric Ton NOx Nitrogen Oxides Nameplate Production Capacity The production capacity of a particular facility based on the expected annual throughput in gallons based upon producing at 100% of design capacity for approximately 330 days per year using a particular feedstock Term Definition Product Offtake Agreement The product offtake agreement exclusively signed with ExxonMobil in April 2019 RD Renewable Diesel RIN or RINs Renewable Identification Numbers to define D4 and D5 RFS Renewable Fuel Standard described in the Energy Policy Act of 2005 enacted by U.S. Congress and administered by the EPA RFS2 The expanded RFS biofuels mandate described in the Energy Independency and Security Act of 2007 enacted by U.S. Congress and administered by the EPA SAF Sustainable Aviation Fuel SusOils Sustainable Oils, Inc., a subsidiary and operating partner of the Company TPA The Term Purchase Agreement with ExxonMobil signed on April 20, 2021 granting ExxonMobil the right to purchase additional renewable diesel from the Bakersfield Biorefinery ULSD Ultra - Low Sulfur Diesel

Thank You

contact@gceholdings.com